Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025

Related Articles: Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

- 1 Related Articles: Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025

- 2 Introduction

- 3 Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025

- 3.1 Understanding the Fundamentals:

- 3.2 Historical Trends and Insights:

- 3.3 Forecasting Mortgage Rate Trends 15 Year Fixed 2025:

- 3.4 Related Searches:

- 3.5 FAQs:

- 3.6 Tips:

- 3.7 Conclusion:

- 4 Closure

Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025

Predicting future mortgage rates is an inherently complex task, influenced by a myriad of economic factors. However, understanding the current market dynamics and historical trends can provide valuable insights into potential rate movements. This exploration delves into the factors shaping mortgage rate trends 15 year fixed 2025 and offers a framework for informed decision-making.

Understanding the Fundamentals:

Mortgage rate trends 15 year fixed 2025 are intertwined with broader economic conditions. Key factors driving these trends include:

- Federal Reserve Monetary Policy: The Federal Reserve, through its Open Market Committee (FOMC), sets the benchmark interest rate, influencing the cost of borrowing across the economy. When the Fed raises interest rates, mortgage rates tend to follow suit, becoming more expensive. Conversely, rate cuts can lead to lower mortgage rates.

- Inflation: High inflation erodes the purchasing power of money, prompting the Fed to raise rates to curb price increases. This can lead to higher mortgage rates.

- Economic Growth: A strong economy generally leads to higher interest rates, as investors demand higher returns for their money. Conversely, a weak economy can lead to lower interest rates as investors seek safer havens for their investments.

- Government Bond Yields: Government bonds, particularly Treasury bonds, serve as a benchmark for other types of debt, including mortgages. When bond yields rise, mortgage rates often follow.

- Housing Market Demand: A robust housing market with strong demand can push mortgage rates higher, as lenders compete for borrowers. Conversely, a weak housing market can lead to lower rates as lenders seek to attract borrowers.

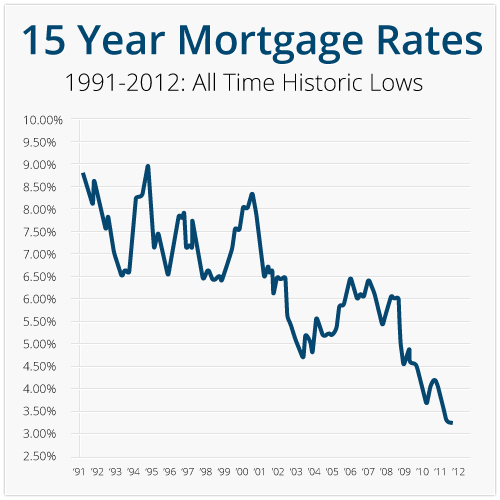

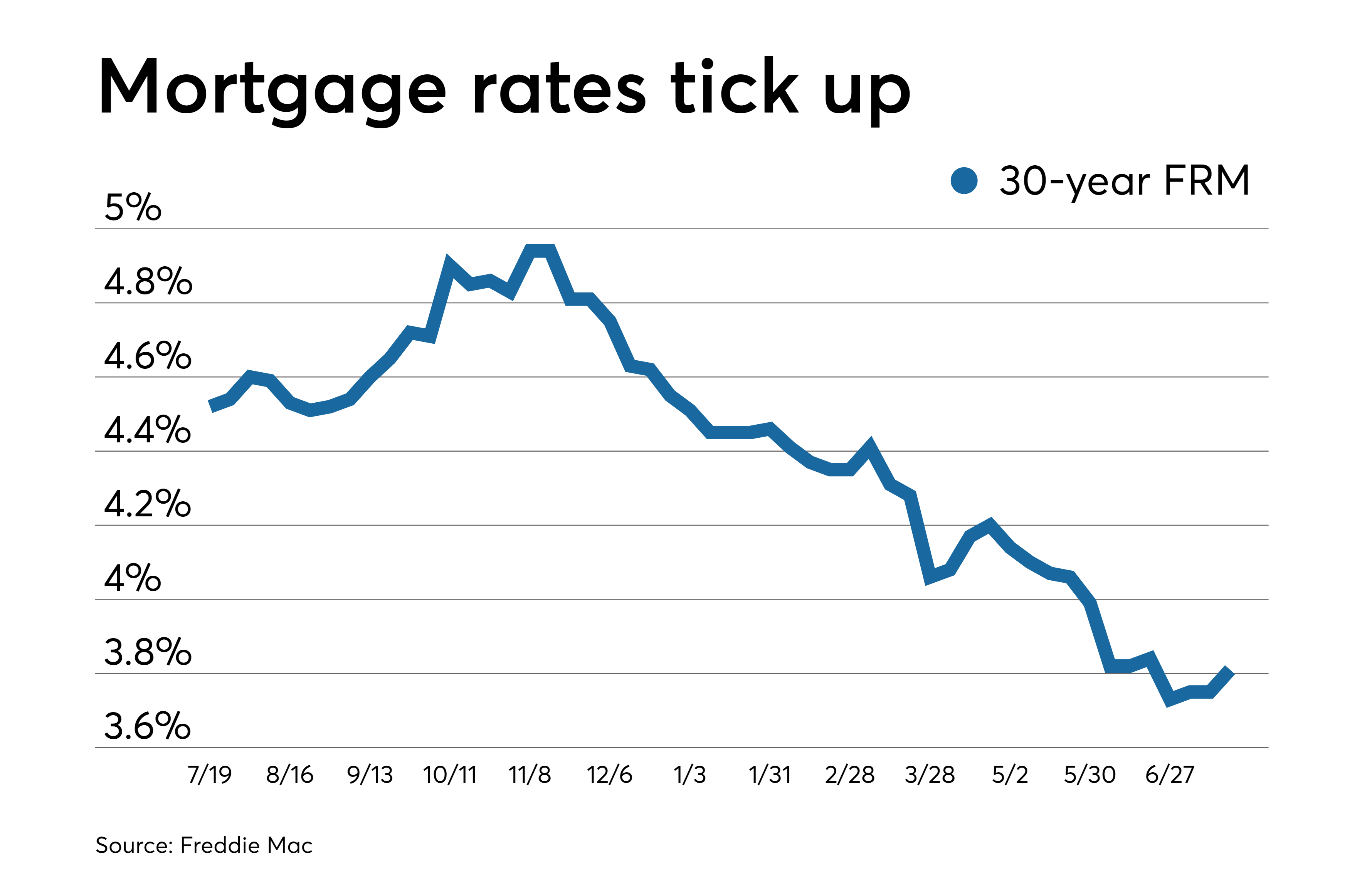

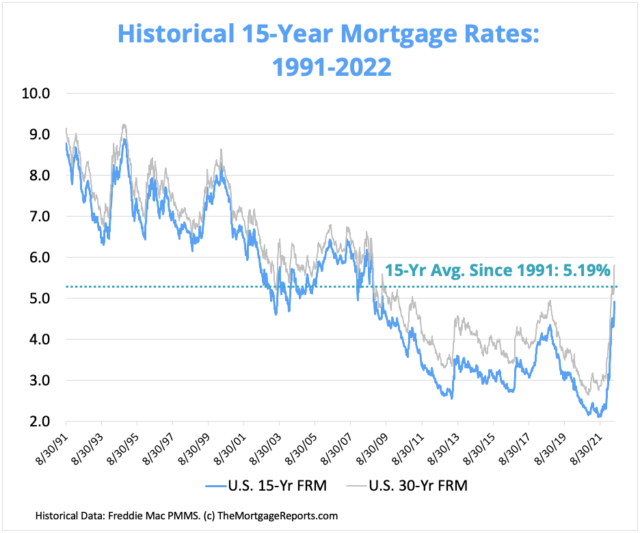

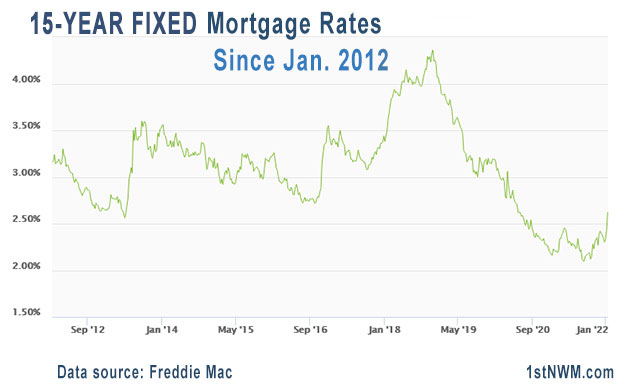

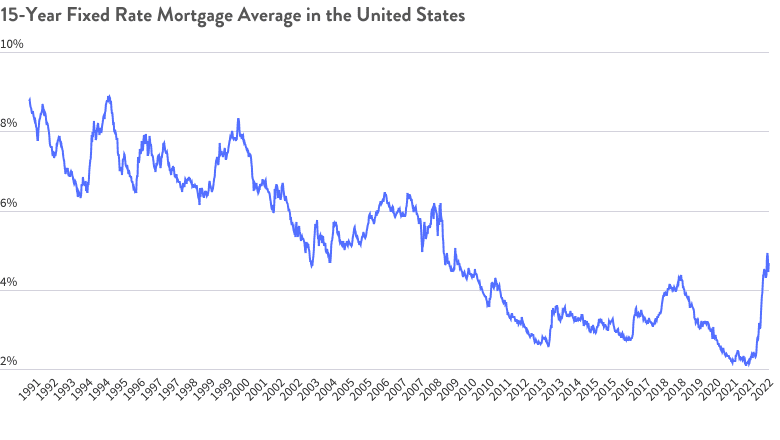

Historical Trends and Insights:

Analyzing historical mortgage rate trends 15 year fixed provides valuable context for understanding potential future movements.

- Long-Term Trends: Over the past several decades, 15-year fixed mortgage rates have generally trended downwards. This is primarily attributed to technological advancements in the mortgage industry, increased competition among lenders, and a shift towards a more efficient financial system.

- Recent Volatility: The past few years have witnessed significant fluctuations in mortgage rates, driven by the COVID-19 pandemic, the subsequent economic recovery, and the Federal Reserve’s aggressive monetary policy tightening.

- The Impact of Inflation: The recent surge in inflation has significantly impacted mortgage rates, leading to a sharp rise in recent years.

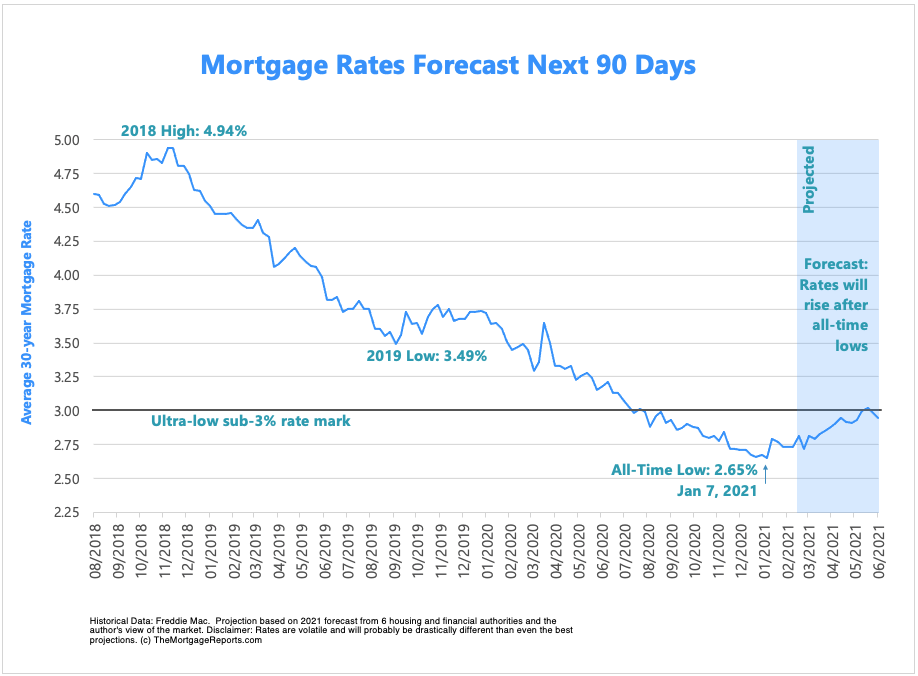

Forecasting Mortgage Rate Trends 15 Year Fixed 2025:

Predicting mortgage rate trends 15 year fixed 2025 requires considering various economic scenarios and their potential impact on the factors discussed above.

- Scenario 1: Continued Inflation and Tightening Monetary Policy: If inflation remains high and the Fed continues to raise interest rates, mortgage rate trends 15 year fixed 2025 could remain elevated or even rise further.

- Scenario 2: Moderating Inflation and Gradual Rate Hikes: If inflation begins to moderate and the Fed adopts a more gradual approach to rate hikes, mortgage rate trends 15 year fixed 2025 could stabilize or even decline slightly.

- Scenario 3: Economic Recession: A recession could lead to a decline in interest rates, as investors seek safe havens for their money. This could result in lower mortgage rate trends 15 year fixed 2025.

Related Searches:

Mortgage Rate Trends 15 Year Fixed 2025 is a multifaceted topic, prompting a range of related searches that provide further insights.

1. 15 Year Fixed Mortgage Rates Today: This search provides real-time information on current 15-year fixed mortgage rates, offering a snapshot of the present market conditions.

2. 15 Year Fixed Mortgage Rate Forecast: This search explores various forecasts and predictions for future 15-year fixed mortgage rates, encompassing different economic scenarios and expert opinions.

3. 15 Year Fixed Mortgage Rate History: Understanding historical 15-year fixed mortgage rate trends provides context for current rate movements and can help gauge potential future directions.

4. Average 15 Year Fixed Mortgage Rate: This search provides data on the average 15-year fixed mortgage rate over a specified period, offering a benchmark for comparison with current rates.

5. Best 15 Year Fixed Mortgage Rates: This search aims to identify the lowest available 15-year fixed mortgage rates from various lenders, helping borrowers secure the most advantageous terms.

6. 15 Year Fixed Mortgage Rate Calculator: This search leads to online calculators that allow borrowers to estimate their monthly mortgage payments based on different interest rates and loan amounts.

7. 15 Year Fixed Mortgage Vs 30 Year Fixed Mortgage: This search compares the benefits and drawbacks of 15-year fixed and 30-year fixed mortgages, helping borrowers choose the most suitable option based on their financial goals and circumstances.

8. 15 Year Fixed Mortgage Rate Trends 2024: This search focuses on the projected mortgage rate trends 15 year fixed for the year 2024, providing insights into potential rate movements in the near future.

FAQs:

Mortgage rate trends 15 year fixed 2025 often raise questions for potential homebuyers and borrowers. Here are some frequently asked questions and their answers:

1. Why are 15-year fixed mortgage rates higher than 30-year fixed mortgage rates?

15-year fixed mortgage rates are typically higher than 30-year fixed mortgage rates because lenders perceive a lower risk in lending for a shorter term. With a 15-year mortgage, the borrower repays the loan faster, reducing the lender’s exposure to potential interest rate fluctuations and default risk.

2. How do mortgage rates impact monthly payments?

Higher mortgage rates result in higher monthly payments. This is because the interest rate determines the amount of interest charged on the loan, which is reflected in the monthly payment.

3. What is the relationship between mortgage rates and home prices?

Higher mortgage rates can lead to a decrease in home prices, as buyers are less willing to pay high prices when borrowing costs are elevated. Conversely, lower mortgage rates can stimulate demand and potentially push home prices higher.

4. Should I wait for mortgage rates to go down before buying a home?

The decision to wait for lower mortgage rates depends on individual circumstances and market conditions. If you are confident in your financial situation and believe that rates will decline significantly in the near future, waiting might be beneficial. However, if you are ready to buy and believe that rates will remain relatively stable or even increase, it might be more prudent to move forward.

5. What are the advantages of a 15-year fixed mortgage?

A 15-year fixed mortgage offers several advantages:

- Lower Total Interest Paid: You pay significantly less interest over the life of the loan compared to a 30-year mortgage.

- Faster Equity Build-up: You build equity in your home faster, as you pay down the principal more quickly.

- Potential for Lower Monthly Payments: While the initial monthly payments may be higher, the shorter term can lead to lower overall monthly payments over the life of the loan.

6. What are the disadvantages of a 15-year fixed mortgage?

A 15-year fixed mortgage also has some potential drawbacks:

- Higher Monthly Payments: The shorter term generally results in higher monthly payments compared to a 30-year mortgage.

- Less Flexibility: You have less flexibility to adjust your budget or make large purchases, as you are committed to higher monthly payments.

- Potential for Higher Interest Rate Costs: If rates decline significantly after you take out a 15-year fixed mortgage, you might miss out on lower interest rates.

Tips:

Mortgage rate trends 15 year fixed 2025 can be navigated effectively with proactive strategies:

- Monitor Market Trends: Stay informed about current and projected mortgage rate trends 15 year fixed by regularly checking financial news sources and websites of reputable mortgage lenders.

- Shop Around for Rates: Compare rates from multiple lenders to secure the most competitive offer.

- Consider a Rate Lock: If you anticipate rates rising in the near future, consider locking in a rate for a specified period to protect yourself from unfavorable rate movements.

- Improve Your Credit Score: A higher credit score can qualify you for lower mortgage rates.

- Save for a Down Payment: A larger down payment can reduce your loan amount and potentially qualify you for lower rates.

- Seek Professional Advice: Consult with a mortgage broker or financial advisor to discuss your individual circumstances and explore the best mortgage options for your situation.

Conclusion:

Mortgage rate trends 15 year fixed 2025 are influenced by a complex interplay of economic forces. While predicting future rates with certainty is impossible, understanding the underlying factors, historical trends, and potential scenarios can empower informed decision-making. By staying informed, comparing rates, and seeking professional advice, borrowers can navigate the mortgage landscape effectively and secure favorable terms for their home financing needs.

Closure

Thus, we hope this article has provided valuable insights into Navigating the Landscape: Mortgage Rate Trends 15 Year Fixed 2025. We thank you for taking the time to read this article. See you in our next article!